According to the Tax Foundation, only six states have an inheritance tax and Kentucky is one of them. This tax should be considered when planning your estate and recognizing tax liability is critical when probating the estate of the deceased.

What is an Inheritance Tax?

So what is an inheritance tax? An inheritance tax is a tax that is imposed on the value of the assets transferred to an heir based on the relationship of the inheritor and the deceased. The closer the relationship, the smaller the tax liability.

The six states with an inheritance tax are Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. In Kentucky, the tax rates vary from 0% to 16% depending on (i) the relationship of the deceased and the person receiving the gift and (ii) the amount of the gift.

What assets are taxable?

In the probate process, we segregated probate property and non-probate property. Non-probate property includes all property of the deceased that passes outside of probate. This distinction, however, doesn’t make an asset immune to the inheritance tax. An inheritance tax will be imposed on any non-probate property that “passes on the privilege or right of succession.” For example, jointly owned bank accounts that are payable-on-death may result in an inheritance tax being due based on the account balance and the beneficiary class of the account’s co-owner(s).

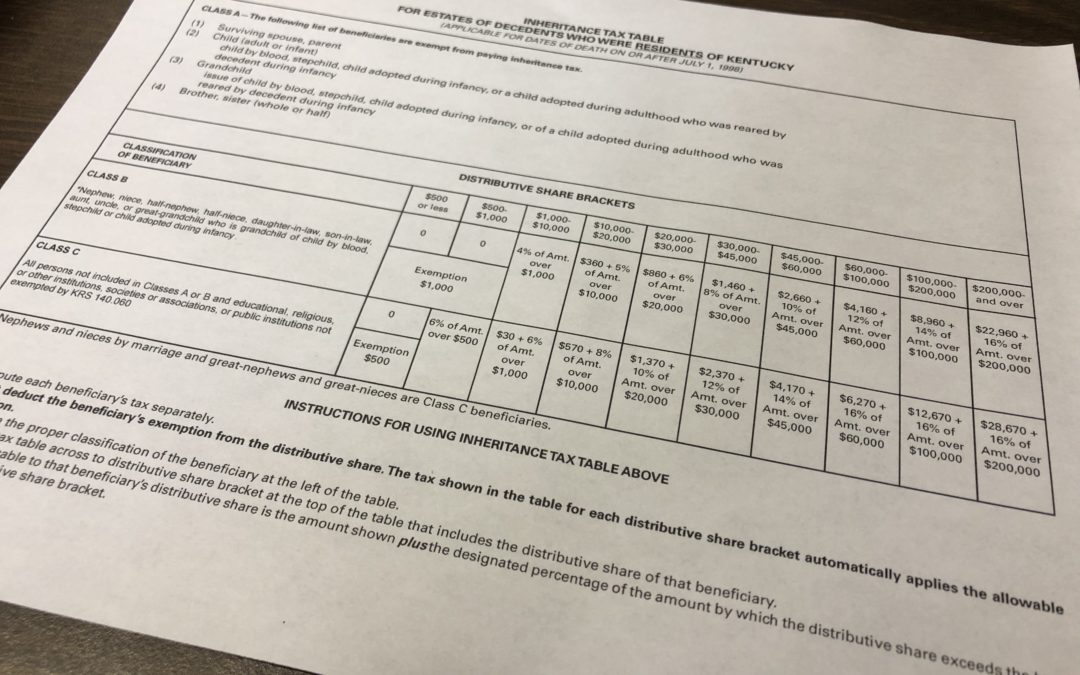

Beneficiary Classes

In determining the amount of tax due on a particular gift, you first must look at the relationship between the deceased and the person inheriting the gift. The relationships are broken down into through groups, or classes.

Class A includes the deceased’s parents, surviving spouse, children, grandchildren, and siblings. Children and grandchildren are generally included if the relationship is one of blood or adoption or if the relationship is the result of a subsequent marriage (stepchildren).

Class B includes the deceased’s nieces and nephews, half-nieces and half-nephews, children-in-law, , aunts, uncles, or great-grandchildren who is grandchild of a child by blood, stepchild, or child adopted during infancy.

Class C includes all persons not in Class A or Class B. Except gifts or bequests made to educational, religious, or other institutions, societies, or associations may be exempted altogether by KRS 140.060.

Once you have determined the beneficiary class, then you can determine the tax liability.

Calculating the Tax

The tax assessed on Class B and Class C beneficiaries varies depending on the amount of the gift. For Class B beneficiaries, gifts are exempt from tax up to $1,000. After the exemption amount is exhausted, the tax is on a sliding scale from 4%-16%. For Class C beneficiaries, gifts are exempt from tax up to $500. After the exemption amount is exhausted, the tax is on a sliding scale from 6%-16%.

The Kentucky Revenue Cabinet has published a convenient Guide to Inheritance and Estate Taxes which includes a tax table on page 6 that helps to calculate the amounts due under Kentucky’s inheritance tax.

A Few Examples

Example 1 – John, a widower, leaves to Susan, his only child, his entire estate. Susan is a Class A beneficiary and this transfer is therefore exempt from paying inheritance tax.

Example 2 – In his will, Joseph makes a $5,000 bequest to Marie, his niece. Marie is a Class B beneficiary and the gift is over the $1,000 exemption amount for Class B beneficiaries by $4,000. The tax rate for gifts of that amount are $4,000 of the amount by which the exemption is exceeded. The tax on Joseph’s bequest to Marie is therefore $160.00.

*Example 3 – In his will, Irene leaves her entire estate to her partner, Jim. Irene and Jim were not married, so Jim is a Class C beneficiary. Irene’s estate – including her home – was valued at $500,000. The tax to Class C beneficiaries for gifts of that size is calculated at “$28,670, plus 16% of the amount over $200,000.” The inheritance tax in this example is $76,670!

As you can imagine, there are nuances to this tax beyond those which can be explained here. If you have additional questions about Kentucky’s inheritance tax please do not hesitate to contact Brackney Law Office, PLLC.